Preparing for IFRS S2 in APAC: Business Strategies for Success – In recent times, ESG-related reporting has evolved further than predicted. Countries around the globe are showing their collective support regarding the commitment, including the global adoption of IFRS S2 (International Financial Reporting Standards Standard 2), which was released in mid-2023 by ISSB (International Sustainability Standards Board). Half the world seems to be preparing mandatory issuance regarding the framework, while the other half is encouraging issuers to progressively adopt. What about APAC?

What’s The Difference Between IFRS S2 and TCFD?

You might have heard of the Task Force on Climate-related Financial Disclosure (TCFD) and its four recommended disclosures: Governance, Strategy, Risk Management, and Metrics & Targets. The TCFD framework may have been incorporated into some parts of your ESG report. However, now you have heard of IFRS S2, which is said to replace TCFD. How much work is it?

IFRS S2 was released in June 2023 and has been ready to be adopted since the beginning of 2024. This standard requires issuers to disclose information on risks and opportunities they encounter and mitigate due to climate change. Issuers are also obligated to disclose general financial reports to portray the solid foundation on which the entity makes decisions regarding risks, opportunities, and resource management.

In its reporting, IFRS S2 requires issuers to inform:

- Climate-related risks to which the entity is exposed, which are: climate-related physical risks and climate-related transition risks.

- Climate-related opportunities available to the entity.

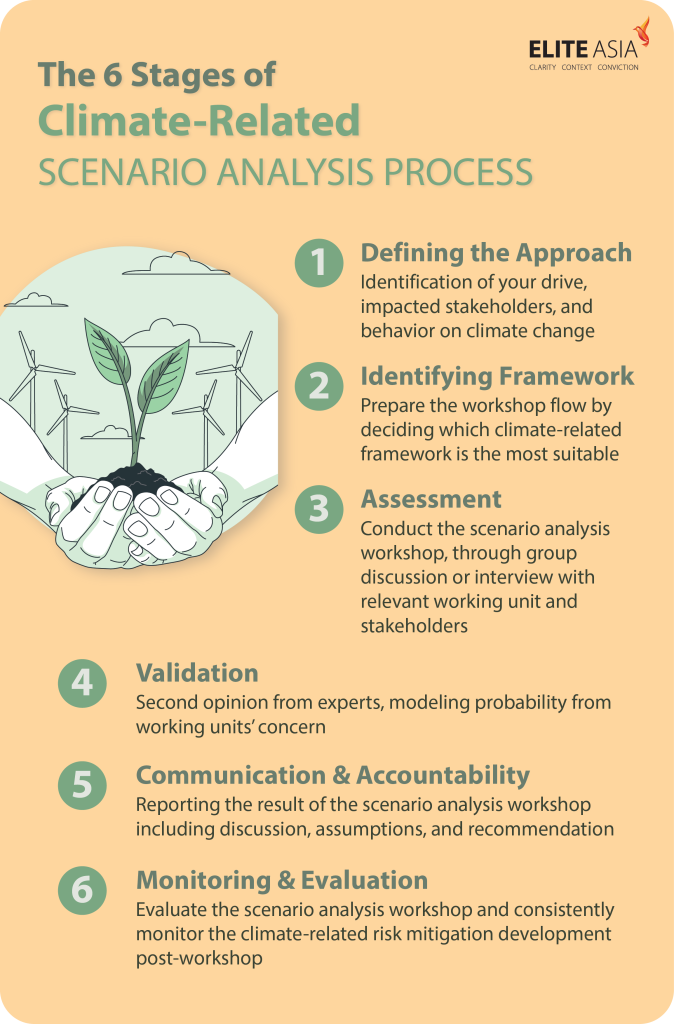

While it seems technically complicated, IFRS S2 aligns with the TCFD with a few adjustments. The general purpose is for stakeholders to understand the issuer’s and entity’s performance in managing their climate-related targets. Therefore, if you have already adopted the TCFD framework for reporting climate-change effects to your organisation, the next thing to do is to conduct a scenario analysis workshop to oversee and mitigate the potential risks and opportunities.

During a scenario analysis workshop, you will undergo a one-on-one focus group discussion session with a related working unit to assess the potential risks and opportunities. Furthermore, you can also conduct a climate risk stress test on your business operation if necessary. The workshop and stress analysis results will be incorporated into your IFRS S2 framework report.

APAC Countries are Preparing for IFRS S2 Adoption

As stated previously, when adopting IFRS S2, there is no one-size-fits-all. Every country has their own consideration and issuance on the adoption, mainly due to self-reflection on readiness and plausibility. However, several countries in Asia have publicly mentioned their participation target in incorporating IFRS S2 or generally mandatory climate-related reporting:

1. Hong Kong

Hong Kong Stock Exchange (HKEX) stated that climate-related disclosure will be mandatory for listed companies starting from the January 1, 2024 reporting period.

2. Singapore

Alongside Hong Kong, Singapore, through Singapore’s Accounting and Corporate Regulatory Authority (ACRA), has mentioned its mandatory issuance for listed companies to incorporate climate-related risk reporting effective April 2025.

3. Malaysia

Bursa Malaysia required main market-listed issuers to report climate-related risks and opportunities. However, they still accept TCFD as a climate-change reporting framework effective December 31, 2025. ACE Market-listed issuers must disclose a basic transition plan to achieve a low-carbon economy effectively by December 31, 2026.

For financial institution issuers, Bursa Malaysia is currently requiring the issuers to produce TCFD climate-related disclosure beginning January 1, 2024.

4. Indonesia

Indonesia is one of the more adaptive countries where issuers have been encouraged to adopt the IFRS S2 early since January 1, 2025. However, TCFD reporting is still sufficient for the next one to two years as the country is still adapting.

Currently, four countries have publicly informed their positions on the IFRS S2 climate-change reporting framework. Though your country has not made IFRS S2 mandatory, we recommend starting ASAP while first-year adoption refreshments are still available.

For any enquiries or quotations about ESG Solutions, get in touch with our ESG Solutions department below: